Consumers striving to be healthy isn’t a new trend. However, how consumers approach their health and wellness has drastically changed. The rise of clean-label, non-GMO, organic and better-for-you products are impacting purchase behaviors across generations. In fact, the Netherlands-based Innova Market Insights notes that savvy consumers making “mindful choices” and seeking “lighter enjoyment” are the Top 2 trends in the beverage marketplace this year.

In its 2017 “Functional Drinks” report, the market research firm reports that 27.2 percent of all beverages launched globally in 2016 featured functional benefits, rising at a compound annual growth rate of 12.6 percent between 2012 and 2016. In 2017, 30.5 percent of all functional drink launches were vitamin/mineral fortified, while 22.8 percent contained high amounts of protein. Rounding out the Top 5 were energy/alertness (20 percent), digestive/gut health (19 percent), and antioxidants (12.7 percent).

Four in 10 U.S. and U.K. consumers have increased their consumption of “healthy foods,” while seven in 10 want to know and understand the ingredient list, the report states. In addition, one in five U.S. consumers are most influenced by “real” ingredients, and the increasingly thoughtful and mindful consumer will continue to catalyze changes in the way companies produce, package and label their products, it adds.

The “lighter enjoyment” trend, which consists of consumers seeking lightness in alcohol content, sweetness, flavor and texture as well as portion size, also is gaining momentum in food and beverages. Better-for-you claims have increased their market penetration from 42 percent in 2012 to 49 percent in 2017, the report states.

In 2016, 75 percent of drinkable yogurt/fermented beverage launches featured a functional health claim, the report adds.

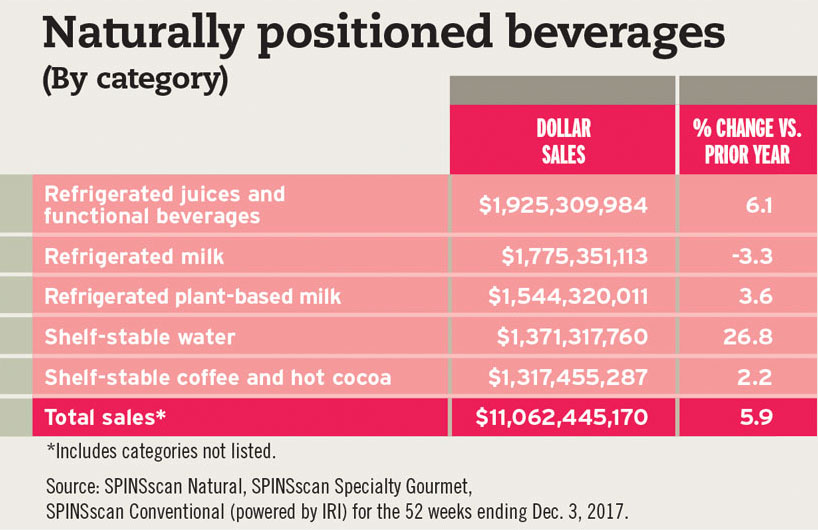

The Top 5 naturally positioned beverage categories by sales for the 52 weeks ending Dec. 3, 2017, according to SPINSscan Natural, SPINSscan Specialty Gourmet, SPINSscan Conventional (powered by IRI).

Among the factors motivating consumers to take health and wellness into their own hands are rising healthcare costs; research linking excessive caloric and sugar intake with health problems including obesity, diabetes and heart disease; and the desire for empowerment and prevention, experts note.

“Additionally, consumers are looking to establish healthy lifestyle routines,” says Kristin Hornberger, principal at Chicago-based Information Resources Inc. (IRI). “This ‘new normal’ is driven by self-care, which encompasses all decisions and activities people make or do, to ensure health and wellness for themselves and their families. Health and wellness is the outcome.

“There is a blurring of lines happening between categories, as traditional health-and-wellness attributes cross into food categories,” Hornberger continues. “Additionally, consumers are looking for solution sets to solve for everyday needs across a variety of categories. Technology will also play a key role in health and wellness and self-care.”

An increased focus on personalization also is motivating consumers to more closely monitor their health and wellness, says Kimberly Kawa, senior nutrition researcher at Chicago-based SPINS LLC.

“Consumers who aren’t getting answers or the results they are seeking through the traditional medical paradigm are trying new and different personalized lifestyles and coordinating health-and-wellness products in the marketplace. There is opportunity for innovation in the functional food and beverage space,” Kawa says. “[Consumers seek] clean-label attributes, including organic, non-GMO and free from artificial flavors, colors or sweeteners; low sugar and/or natural alternative sweetener use; functional ingredient content; and probiotics.

“Consumers who follow certain diet tribes seek out specific ingredients to avoid or include,” she continues. “While there certainly is some overlap, a one-size-fits-all approach is becoming an antiquated concept.”

Sarah Schmansky, vice president of growth and strategy at New York-based Nielsen, also points to this trend.

“Today’s shoppers are making more focused purchase decisions. For starters, choice is omnipresent and brand messaging permeates all facets of our lives,” Schmansky says. “Consumers are increasingly mindful about what they’re putting in their bodies. The ‘why’ and ‘how’ behind the products have become as important as the product itself, oftentimes becoming the primary decision-making criteria that drives a purchase. This has added an entirely new layer of complexity to the way fast-moving consumer goods companies develop and market products to consumers.”

Schmansky adds that the lion’s share of total beverage dollars includes products that are free from artificial colors and contain all-natural ingredients. “However, products with only one to five ingredients, are free from GMOs and contain coconut as an ingredient are on the rise,” she says. “Beverage products that are emerging with rapid dollar growth compared to a year ago are those with attributes of a low glycemic diet (up 49.7 percent) and probiotic beverages (up 82.1 percent).”

Americans are expecting more from their drinks, says Kevin Weissheier, consumer insights executive at New York-based Kantar Worldpanel. “They are looking for not only health-benefit beverages, such as smoothies and [high-pressure processed] juices, but also ones that cleanse or purify, such as bottled water. All three of these beverage categories have seen tremendous growth.”

Gary Hemphill, managing director of research at New York-based Beverage Marketing Corporation (BMC), notes that the heightened importance of health-and-wellness beverages has paved the way for more industry innovation, which is resonating with today’s consumers.

“Bottled water is the category that has benefited the most from [the] consumer movement to health-and-wellness beverages — so much so that it is the most popular beverage in the U.S. today,” Hemphill says.

In addition to the ascension of water, IRI’s Hornberger says that ready-to-drink tea is appealing to health-conscious consumers. “Water, even when sweetened and flavored, benefits from the healthy halo of pure water — nature’s ideal beverage,” she says. “Tea offers a similar halo and provides a platform for exotic/premium additions like kombucha and matcha.”

Function first

In 2018, fortified/functional (FF) foods and beverages will continue to proliferate in the marketplace, and experts predict a continued rise in foods and value-added beverages that tout health benefits and functionality.

In its May 2017 report titled “Fortified/Functional Beverages in the US,” Chicago-based Euromonitor International highlights that “many of the bestselling FF beverages continued to stem from sports drinks and energy drinks, where products are typically fortified/functional by definition.”

The Top 5 USDA-certified organic beverage categories by sales, according to SPINSscan Natural, SPINSscan Specialty Gourmet, SPINSscan Conventional (powered by IRI)

Beverages touting natural attributes netted sales of more than $11 billion, a 5.9 percent increase, while organic beverages generated $3.1 billion in sales, a 5.4 percent increase, during the same time period, SPINSscan data indicates.

Breaking down the organic beverage category even further, organic shelf-stable functional beverages and organic RTD refrigerated teas and coffees saw double-digit growth of 44.6 percent and 43.2 percent, respectively, according to SPINSscan data.

Among the categories appealing to health-conscious consumers are coconut water and other plant-based products. Kombucha also is benefiting as gut health continues to be a focus with bacteria-rich products growing in popularity, especially because kombucha brands now can be found in multi-outlets and conventional supermarkets, SPINS’ Kawa says.

Indulgent beverage categories also are breaking mainstream formulation norms in the name of health and wellness. “Your typical ready-to-drink mocha latte can now be found dairy-free and lightly sweetened,” Kawa says. “Your cloyingly sweet cocktail mixer is now a naturally positioned, functional, herb-infused, low-calorie cocktail or mocktail mixer. There is innovation happening in every beverage segment to meet the consumer where they are on the preference spectrum.”

Craft sodas also have benefited from the health-and-wellness trend as they tout the use of natural ingredients made in local regions, says Chrystalleni Stivaros, industry research analyst at Los Angeles-based IBISWorld.

“Better-for-you products have expanded the beverage industry,” Stivaros says. “Beverage manufacturers are taking advantage of this new trend by creating products with natural ingredients. Craft sodas are considered to be premium goods, or goods made with higher quality ingredients, which command higher prices, benefiting the industry.”

Trimming the fat

Nearly 2 billion adults worldwide qualified as overweight in 2016, and 650 million are obese, according to the World Health Organization, while the Centers for Disease Control reports that 30.3 million Americans have diabetes, including nearly 24 percent of the U.S. population who are undiagnosed.

“Research linking excessive caloric and sugar intake with health problems such as obesity and heart disease motivates consumers to monitor their health and wellness,” Stivaros says. “In response, [consumer packaged goods] companies are reformulating products to cater to shifting demand.”

Additionally, 75 percent of consumers say that a nutritious diet is important to how they achieve a healthy lifestyle, according to research from the National Association of Convenience Stores, Alexandria, Va.

However, experts note that different demographics define health and wellness differently.

Tea benefits from a simple clean label and healthy attributes. Bigelow Tea introduced a new line of bagged teas: Bigelow Benefits. The line consists of everyday teas that support well-being with good-for-you ingredients, the company says. (Image courtesy of Bigelow Tea)

“For some, it is all about calories; for others, sugar; for others, having more natural ingredients; and so on,” BMC’s Hemphill explains. “Beyond this, there are demographic differences as well. What’s important from a health-and-wellness perspective can vary by sex, age and even ethnicity.”

Nielsen’s Schmansky also notes that the interest and purchase of health-and-wellness products can vary by income level and age group. “Across generations, millennials and Generation X consumers are more likely to seek out and purchase products that are labeled organic, free of GMOs and don’t include added hormones,” she explains. “Comparatively, members of the Greatest Generation place less importance on these claims. Demographic groups [that] influence the forward movement of this trend include consumers under the age of 35, those with annual household incomes over $100,000 and families with children.

“They’re leading the way with respect to buying products they believe are better for them, their families and the planet,” she continues. “They care much more about transparency and clean label than older generations do, and their spending prowess is growing.”

Kantar Worldpanel’s Weissheier notes that consumers older than 50 are more focused on health concerns that directly impact ailments and are looking for products that are low acid, vitamin fortified and fiber enriched. On the other hand, millennials are emphasizing the “process of their beverage” and stressing organic and all-natural health needs as well as antioxidants.

“Millennials are passing these same values down to their centennial children, who are the future consumers of America,” Weissheier says.

In line with health-and-wellness trends, better-for-you claims are driving growth in the beverage industry, Schmanksy says. “For example, in the 52 weeks ending Aug. 19, 2017, total beverage dollars grew 1 percent. However, beverage products that are free from GMOs or only contain one to five ingredients saw higher growth than the total category (up 6.3 percent and 3.5 percent, respectively),” she says, citing Nielsen Product Insider data. “In addition, beverages that are ‘free from artificial colors’ own 46 percent of total beverage share (a 1.4 percent dollar growth), while those with ‘all-natural ingredients’ own 34 percent of total beverage dollar share (a 2.1 percent dollar growth).”

“Consumers are looking to always improve their lives, whether it is through technology, exercise, food and/or beverages. By adding these new layers to the beverage sector with these ‘super-categories,’ consumers are able to become even healthier without any major life changes. Consumers believe that they can become healthier by engraining ‘healthy f luids’ into their lives. From what we’ve seen and expect, health and wellness will become one of the single largest drivers in the beverage space for the future. Beverages are no longer opportunities for constant indulgence — they are an integral dietary piece, which will only grow in importance.”

— Kevin Weissheier, consumer insights executive at Kantar Worldpanel

Smoothies are the “undoubtable winner” of the better-for-you, healthy indulgence movement, Weissheier says. “Younger consumers are driving the fruit and sweet smoothie growth, while millennials are more engaged with the green and veg variants,” he says. “Smoothies allow a ton of room for adding in … even healthier options such as collagen protein, whey and chia seeds.”

Experts expect that better-for-you beverages with simpler ingredients and free-from labels will continue to impact the beverage industry for many years.

“Consumers are actively seeking products that have an absence of negatives (e.g., no artificial colors) and a presence of positives (e.g., organic),” IRI’s Hornberger says. “Additionally, consumers are looking for solution sets and also [are] shopping multiple different categories to comprehensively meet their health-and-wellness needs.”

Kantar Worldpanel’s Weissheier adds: “Consumers are looking to always improve their lives, whether it is through technology, exercise, food and/or beverages. By adding these new layers to the beverage sector with these ‘super-categories,’ consumers are able to become even healthier without any major life changes. Consumers believe that they can become healthier by engraining ‘healthy fluids’ into their lives. From what we’ve seen and expect, health and wellness will become one of the single largest drivers in the beverage space for the future. Beverages are no longer opportunities for constant indulgence — they are an integral dietary piece, which will only grow in importance.” BI