Between Drinks

RTD alcohol retains popularity across on-premise

Consumers seek quality, variety of flavors from drinks

Image courtesy of Monaco Cocktails

In the age of streaming, where viewers can access some of the best movies around, from blockbusters to award-winning films to the critically acclaimed, sometimes it’s hard to justify the price of going to the theater.

Yet, where streaming from home is convenient and affordable, there is something to be said about going to the movies. The screen is larger and clearer, and let’s not forget theaters have a bigger speaker system. And then there’s the experience of getting out — being in the presence of other people — where movie watching becomes a collective experience.

Similarly, in the world of beverages, although consumers have an abundance of ready-to-drink (RTD) alcohol options to enjoy in-home, interestingly, the on-premise sector serves as a crucial avenue for consumers seeking to engage with the category.

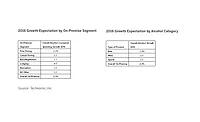

In a recent CGA Powered by Nielsen IQ report, titled “Who is the American RTD Drinker?,” Andrew Hummel, CGA client solutions director of Americas, analyzes CGA’s latest research, noting that data from CGA OPUS shows that RTD alcohol is retaining its position as a popular and successful beverage category across the American on-premise.

“Indeed, CGA’s research shows that 17% of American drinkers who visit bars, pubs and restaurants have consumed RTD alcohol in the past three months,” Hummel says. “Seasonal figures collected over the past two years also suggest that RTD consumption is consistent across seasons.

“Between fall 2021 and the following spring, consumption sat stable at 18% of all on-premise users,” Hummel continues. “The figure experienced a slight drop of two percentage points in the fall of 2022, only to increase to 17% in the spring of the following year.”

As a significant majority of 75% of all RTD consumers dine out at least once a week, almost half visit on-premise venues with the primary intent of consuming alcohol, Hummel notes.

“Additionally, 40% of individuals consume RTDs in both food- and drink-led scenarios, while the remaining portion is evenly divided between those who prefer RTDs while dining out or drinking out exclusively,” he says. “Around a quarter enjoy RTDs while watching sports, as a regular everyday beverage, or during after-work drinks.”

Meanwhile, approximately 20% of individuals place a premium on brand recognition, with nearly as many always choosing their favorite brand, according to CGA’s research.

“This consumer preference is reflected in brand loyalty figures, which our research suggests to have remained relatively stable over the past two years,” Hummel explains. “However, our OPUS data also indicates that 18% of consumers are actively seeking out new RTD brands and a smaller segment can be tempted by increasing product visibility on the bar or in fridges, showing that some RTD drinkers are still keen to try new brands.

“When promoting unfamiliar brands, manufacturers and suppliers need to account for the large majority ― a remarkable 56% ― for whom quality is paramount,” he continues. “The range of flavors available come as a relatively close second with 48% of RTD drinkers looking for a variety of expressions, meaning that there are plenty of innovation opportunities for manufacturers within the RTD category.”

Further, Hummel points to the type of alcohol used — malt, sugar or spirit — as approximately one-third of consumers choose RTDs based on the type of base-alcohol used.

“Among white spirits, vodka is by far the most popular (70%) while tequila’s popularity, selected by over half of RTD consumers, aligns with wider consumer trends in the country,” Hummel says. “Rum is a very popular base alcohol, selected by 42% of RTD drinkers while gin is the least appealing white spirit base (30%). Meanwhile, whiskey (43%) is almost twice as desirable as brandies and cognac (23%).”

As the popularity of RTD alcohol shows no signs of abating, it appears that manufacturers, suppliers and operations have an opportunity to harness the category’s potential across the American on-premise.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!