Special Report: CSDs

2021 Soft Drink Report: New CSDs crafted for ‘sizzle and pop’

Cream soda sees triple-digit growth

In Taylor Swift’s 2014 lead hit single “Shake It Off,” she sings about “players gonna play, play, play, play, play, And the haters gonna hate, hate, hate, hate, hate,” but “Baby, I'm just gonna shake, shake, shake, shake, shake — shake it off.” After a tumultuous year of lockdown, mask-wearing and restaurant and bar closures, beverage manufacturers, distributors and consumers also are “shaking off” the doldrums and hoping to return to normalcy.

Many beverage categories such as juice and juice drinks, still and sparkling water, beer, wine and spirits saw double- and even triple-digit surges in performance amid the pandemic. While carbonated soft drinks (CSDs) had previously lost ground to better-for-you (BFY) beverages such as bottled water, the $30.5 billion CSD category grew 11.4 percent in multi-outlets for the 52 weeks ending Jan. 23, according to data from New York-based Nielsen.

Chicago-based Mintel’s May 2020 “Carbonated Soft Drinks: Incl Impact of COVID-19 – US” report also points to “riding on the heels of two years of category growth … expected to extend into 2021.” The report notes that the mature, top-heavy category is largely dominated by two major players, The Coca-Cola Co., Atlanta, and PepsiCo, Purchase, N.Y., who have been the catalysts for growth largely attributed to successful flavors, BFY products and packaging innovation.

“In the challenging economic times that may lie ahead, while value-focused offerings may seem like an alternative, brands are insulated by familiarity, dedication and complex, solid distribution channels. The top-heavy carbonated soft drink category has a unique advantage in this equally unique time: deeply rooted connections with not only their most engaged fans, but also with less frequent users,” the report states. “Decades of legacy brand building centered not only on refreshment and enjoyment, but also community and family, are likely paying off in spades as consumers crave comfort, normalcy and nostalgia.”

Yet, Jacqueline Hiner, lead analyst for New York-based IBISWorld Inc., suggests that products that support health and wellness are taking share away from carbonated soft drinks.

“Overall, declines in high-fructose corn syrup and sugar consumption and growth in healthy eating have continued to pressure sales according to our research,” Hiner explains. “Although there has been some support from carbonated waters, as well as a surge in demand during the pandemic, this has not been enough to make up for declines in traditional sugary CSDs.

“… Meanwhile, demand is rising for specialized products or those that are made with less processed ingredients, such as craft sodas made with cane sugar or carbonated beverages that lack sweeteners altogether such as Spindrift,” she continues. “CSD producers have increasingly released heathier products to appeal to increasingly health-conscious downstream markets.”

The sweetener sources for CSDs also are changing. Producers are opting for the use of fruit juice and plant-derived sweeteners like stevia in products. For instance, Coca-Cola has increased the use of the natural low-calorie stevia in CSDs as opposed to most low-calorie and diet sodas sweetened with aspartame, an artificial sweetener, Hiner notes.

Cream of the crop

When it comes to flavors and sales growth, cream soda is No. 1 in multi-outlets, with $406 million in sales and triple-digit growth of 116 percent in multi-outlets for the 52 weeks ending Jan. 23, Nielsen data reports. Albeit from a much smaller volume, ginger beer rung up $147 million in sales with 36 percent growth; and assorted flavors, at $62 million, registered a year-over-year increase of nearly 23 percent.

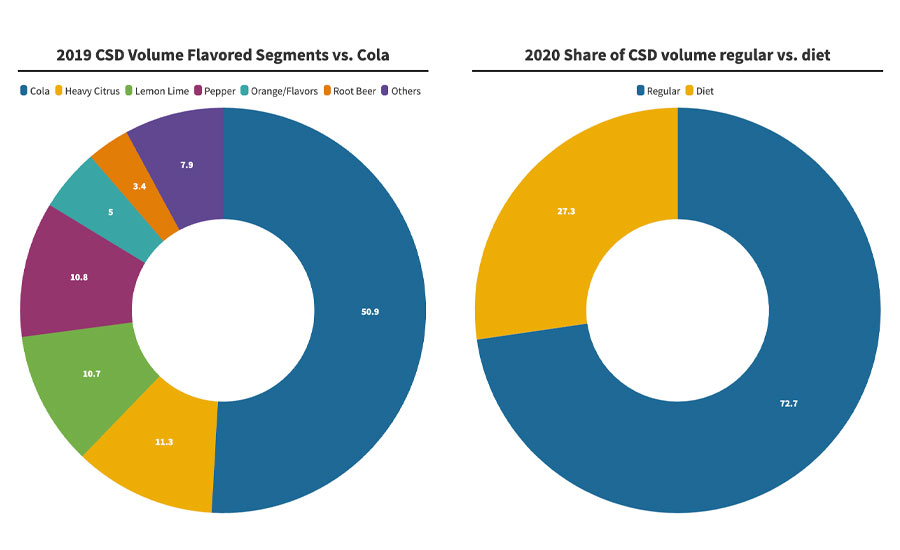

For the same timeframe, Cola was the largest sub-segment, with sales of $13 billion, an increase of 12.6 percent; Citrus, at $4.6 billion and an 8.7 percent increase; Pepper, which saw a 12.2 percent increase and sales totals of $3.4 billion; Lemon Lime with sales of $2.9 billion, a 12.8 percent rise; and Ginger Ale saw sales of $1.4 billion, an increase of 13.2 percent.

Ilana Orlofsky, senior marketing manager at Imbibe, Niles, Ill., suggests it will take a long time before the core CSD flavors — cola, root beer, orange, lemon/lime and citrus — aren’t the top performers.

“But we’re definitely paying attention to some flavor profiles that we expect to gain in popularity in the next several years. Cucumber, sometimes paired with another fruit, has a lot of potential, especially because the crisp and fresh profile performs well in a cocktail or mocktail, which we know many consumers have been building at home in the past year,” Orlofsky says. “New Wave Soda has a cucumber soda. Dry Soda also has a cucumber offering in their adult-friendly, low-sugar soda line, as well as lavender, blood orange, watermelon, Fuji apple, ginger and Rainier cherry.”

Other flavors to watch include blood orange as one of the “sexier citrus fruits,” along with coconut as used in the Toasted Coconut variety from United Sodas of America, which is reminiscent of Malibu Rum, but without the rum, of course, she adds.

When it comes to flavor, beverage companies are striving for more “sizzle and pop” innovation within the CSD category. Earlier this year, the Coca-Cola Co. released Coca-Cola with Coffee and Coca-Cola with Coffee Zero Sugar. Infused with Brazilian coffee, the full-sugar variety is available in three signature flavors, Dark Blend, Vanilla and Caramel, while the zero-sugar counterpart comes in Dark Blend and Vanilla. All the hybrid beverage varieties are shelf-stable and contain 69 mg of caffeine in each 12-ounce slim can.

Noting that CSDs are a massive category — the second largest beverage category in the country on a volume basis, Gary Hemphill, managing director of research at New York-based Beverage Marketing Corporation (BMC), suggests that the category has struggled of late because consumers are moving toward healthier refreshment and craving variety.

Although volume sales of CSDs has been sluggish for a few years, CSDs have been further impacted by the pandemic, more so than other refreshment beverage categories, Hemphill says.

“The category was hit harder than most by the shutdowns of restaurants and other on-premise establishments,” he says. “We’re forecasting another decline in carbonated soft drink volume in 2021.”

Yet, Jennifer Mapes-Christ, publisher of food and beverage research for Packaged Facts, Rockville, Md., details that shifting consumer patterns and interest in at-home cocktail making are bolstering CSD interest.

“All this home consumption has led to increased desire for novelty, as consumers might have discovered new flavors or be otherwise shaken out of their beverage routines at a restaurant or bar,” she explains. “This has left consumers willing to seek out new flavors and try new beverages, including new carbonated types. More beverage companies are offering suggestions for how to use their products to make cocktails or mocktails, with interest in the latter boosted by younger consumers’ interest in the fun of cocktails without the alcohol.”

In the to-go sector, many restaurants and bars have switched to offering individual packages of soft drinks over using fountain options. “Furthermore, some consumers saw sealed bottles and cans as more hygienic in an era of concern about people coming into contact with our food and beverages,” Mapes-Christ notes.

Mixing it up with variety packs

Within the burgeoning production of CSDs, experts recommend plenty of flavor innovation as an industry mainstay. “Overall, innovation is key to keeping the category fresh and top-of-mind with consumers,” BMC’s Hemphill says.

Similarly, Packaged Facts’ Mapes-Christ notes that consumers are looking for innovative flavors and variety. “Seasonal and limited-edition flavors appeal to it,” she explains. “Consumers are also looking for a way to get a boost in their day and varieties that blur into the energy drink category are a way for consumers to get that from flavors not associated with coffee.”

Craft soda brand Jones Soda Co., Seattle, introduced its first mass-market variety 12-packs, as well as a rotating series of special flavors that will change every six months. The new 12-packs include a Fan Faves Variety Pack bundling Jones’ top-selling Cream Soda, Berry Lemonade, Orange Cream and Green Apple flavors; and a Mixer Variety Pack containing Jones Cola, Lemon Lime and Ginger Beer targeting today’s craft cocktail and at-home DIY trends. Both packs take advantage of value pricing and pantry stocking behavior, the company says.

Additionally, the first drink in the Special Release series is Jones Special Release Birthday Cake Soda, an exclusive flavor created for the brand’s 20th anniversary in 2016, was revived for its 25th anniversary. Available from January through June, the limited-release Birthday Cake Soda will then be replaced with Jones Special Release Pineapple Cream, which will be available from July through December. Both flavors are frequently requested by the brand’s fans because of their fun, innovative and only-from-Jones’ taste profiles, it says.

Bubbling over with functionality

As consumers strive to reduce sugar and boost their health, functional beverages that hydrate, energize, and boost immunity and gut health now are mainstream in the beverage industry. They also are permeating the soda category.

United on the importance of gut health, Olipop Co-founders David Lester and Ben Goodwin, who launched Obi Probiotic Soda in 2013 and sold it a few years later, launched their ready-to-drink (RTD) functional soda in 2018. The Oakland, Calif.-based BFY beverage provides consumers with a healthy, delicious substitute for soda that also boosts digestive health, it says. The product is sold at nearly 5,000 grocers and convenience stores nationwide including Whole Foods, Sprouts, Safeway, Kroger, Fresh Market and Wegmans, as well as direct-to-consumer on www.drinkolipop.com.

“One can of Olipop has between 2 and 5 grams of sugar, 35-45 calories, and 9 grams of prebiotic fiber scientifically proven to support digestive health,” Lester explains.

The co-founders recognize the importance of meeting consumers where they are. “People love soda, and it isn’t our goal to take anything away from the experience of consuming and enjoying it,” Goodwin explains. “Olipop is a soda, and it's also a nutritional supplement in the form of something delicious and familiar. It tastes great, and consumers have responded wonderfully to being able to use Olipop as a tool that easily incorporates key nutrients into their diets.”

Noting that CSDs are not the only beverages containing the fizziness of bubbles, Packaged Facts’ Mapes-Christ points to the increasing introduction of flavored seltzer waters for boosting the category. “More consumers are looking for ways to reduce the sugar in their diet and these beverages offer consumers a way to enjoy their bubbles without added sugar,” she says. “… Consumers are increasingly looking for health benefits in their beverages also. Carbonated soft drinks that features nootropics are positioned as a better-for-you beverage and an alternative to traditional caffeine-based beverages.”

Increasingly carbonates are being used as cocktail mixers. Noting the growth of the mixer category, on March 1, PepsiCo launched its Neon Zebra line in four non-alcohol flavors: citrus-flavored Margarita mix, strawberry-lime-flavored Strawberry Daiquiri mix, lime-mint-flavored Mojito mix and a lemon-flavored Whiskey Sour mix, the company says.

The CSD market also will benefit from hybridization that continues to proliferate throughout the overall beverage market. BMC’s Hemphill states: “Beverage hybrids have been increasing in numbers, and the CSD category is no exception. We’ve seen energy CSDs and more recently coffee CSDs as just a couple examples. We’re likely to see more hybrids where they make sense and are likely to resonate with consumers.”

IBISWorld’s Hiner agrees: “The most prominent form of hybridization in the industry is the proliferation of energy soft drinks. Many companies have been launching CSDs with added caffeine, such as Coca-Cola Energy. Other companies have been similarly expanding energy lines.

As for the category’s future, Mintel’s report forecasts that the CSD market will grow anywhere from 0.4 percent to around 2 percent year-over-year between 2021 and 2024 with sales of $40.4 billion in 2024.

In the midst of new economic uncertainties and hurdles, Kaitlin Kamp, Mintel’s food and drink analyst, believes that in-home consumption and even indulgence will result in sustained growth for CSDs.

“The way forward for all types of brands is to inspire consumers to rediscover ways to enjoy CSDs all over again, with new recipes, times and occasions, especially riding the tailwinds of other dayparts getting a boost, like mealtime and cocktail hour,” Kamp says.

Similarly, IBISWorld’s Hiner notes that the category can continue to evolve and “shake things up” by increasing its focus on healthier beverages, including unsweetened carbonated waters or those sweetened with fruit juice. “As these products emerge and continue to grow in popularity, the industry as a whole can regain market share,” she says.

Although there’s been talk of soda’s decline for many years, it still is a $40 billion category, Olipop’s Lester notes. “Nearly half of all American adults drink at least one glass of soda per day. It’s a category that consumers love and it has deep emotional and cultural resonance,” he says. “[T]he future of the category is function, [which is] ironic in some ways because that’s how it started. Within the next decade, consumers will be asking ‘this is delicious, but what does it do for me?’”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!