Amazon’s acquisition of Whole Foods Market impacts industry

Beverages No. 4 in organics market

In August, Seattle-based Amazon finalized its $13.7 billion acquisition of natural and organic retailer Whole Foods Market, Austin, Texas. The acquisition has translated into big changes not only in the pricing of many natural and organic products sold within Whole Foods stores, but likely will impact the ways that consumers purchase consumer packed goods (CPG).

The grocery price war is going to heat up, according to Chicago-based Euromonitor International’s Head of Retailing Michelle Grant in a June blog post titled “The Implications of Amazon’s Acquisition of Whole Foods.” “Grocery is the largest consumer category in the U.S., and it enjoys a high purchase frequency. Amazon has always had an eye on grocery for these reasons,” Grant stated in the blog post. “It can’t be the ‘Everything Store’ without being dominant here.”

Grant noted that the eCommerce distributor began its grocery journey in 2007 with AmazonFresh, expanding with various platforms, programs and brick-and-mortar pick-up locations earlier this year. “This acquisition means that Amazon now owns roughly 460 stores to accelerate its growth in the grocery channel,” she added.

As a result, new delivery models could be coming to Whole Foods and there’s a strong possibility that Instacart, the white-label delivery partner for Whole Foods, will be replaced with one of Amazon’s programs, Grant wrote. “While Prime Now replicates the Instacart experience with one- to two-hour delivery with products picked from grocery stores, I think that AmazonFresh will simply add a hyperlocal delivery element to remain as Amazon’s main grocery brand.

“I also speculate that Amazon could put AmazonFresh Pick Up stores in the parking lots of Whole Foods where possible or locate them as standalone options near the stores so the stores can serve as fulfillment centers for Pick Up stores,” she continued. “The other option is to expand Whole Foods’ existing click-and-collect program.”

Pricing of food and beverages in the overall natural and organic channel also is likely to be impacted by the acquisition of Whole Foods by Amazon, experts say. Private-label brands such as 365 by Whole Foods, and the fact that Bentonville, Ark.-based Wal-Mart Stores Inc.’s private-label brands now can be purchased online following the acquisition of Jet.com Inc. in 2016, are further impacting the channel, they add.

“With Amazon and Whole Foods merging, we’ll see prices dropping for sure, and if the more premium beverages in this space can’t compete at a price point Amazon demands, they will either drop out, go direct to [the] consumer or reformulate to be cheaper,” says Kara Nielsen, sales and engagement manager of USA at the Netherlands-based Innova Market Insights.

David Lummis, market analyst for Rockville, Md.-based Packaged Facts, also echoes those sentiments. “With more than 300 million customer accounts on Amazon.com, Amazon is a huge engine for getting consumers to order online. The trick will be if they can be successful with perishables, which is a big part of the natural and organic channel,” he says. “But the impact is enormous. Just a few days after the deal was closed, they announced they were cutting prices on a large selection of products in store.

“Slightly discounted Amazon Echos and Echo Dots are now on sale at Whole Foods, providing physical touchpoints for Amazon while spurring trial and engagement,” he continues. “Other grocers are courting Amazon. Using brick-and-mortar stores for pick up is a key driver for the channel.”

Going mainstream

As a result of increased consumer focus on transparency, claims like natural, organic and gluten free are becoming more common in CPGs, experts note. The natural and organic channel, which includes retailers like Whole Foods, Trader Joe’s, Earth Fare, Fresh Thyme Farmers Market and Natural Grocers, continue to experience growth.

Natural products, once found only in natural retailers, have “broadened terrifically” into conventional grocery, convenience, box stores and the like, indicating consumer demand from every quadrant, including millennials, Kara Nielsen says. This also has led to increased sales.

Dollar sales of natural products sold in U.S. multi-outlets for the 52 weeks ending July 1 were $43.7 billion, a 6 percent increase compared with the prior year, while sales of organic products were nearly $17.1 billion, a 10.6 percent increase for the same timeframe, according to New York-based Nielsen.

In an August Insights report titled “What it means to be ‘clean’ in today’s [fast-moving consumer goods] (FMCG) market,” the market research firm notes that transparency and clean label claims aren’t just providing insight — they’re driving sales.

“For example, sales of products that make organic claims are up 10 percent from a year ago, sales of products that make ‘all natural’ claims are up 7.8 percent and sales of products that claim ‘no additives or artificial ingredients’ are up 8 percent,” it states. “We can also see increased sales across the broader categories along the progressive scale that describes the attributes within the clean arena.”

Innova Market Insights’ Kara Nielsen also points to the clean-label trend. “In our 2017 Top Trends, Clean Supreme is our top trend, indicating that clean-label products (what were once found in the natural channel) are mainstream, and that the label has gone beyond just the natural and no additives/no preservatives space into transparency, clean colors and more,” she says. “Clean, including non-GMO, products more and more often are expected and mass manufacturers have responded.”

Beverage brands also are releasing new products with natural, organic, non-GMO and no additive/preservative claims. In a May report titled “Organic Beverages in the US,” Chicago-based Euromonitor International highlights the growing number of organic sub-brands launching as part of already well-established household brands. “In 2016 alone, organic extensions of Gatorade (sports drink), Pure Leaf (ready-to-drink tea) and Capri Sun (juice drink), to name a few, showed manufacturers’ commitment to their core brands and their understanding of where consumer interest is directed,” the report states.

Steady growth

The Washington, D.C.-based Organic Trade Association’s (OTA) Senior Writer/Editor Barbara Haumann also notes that consumer desire for these product attributes has translated into steady growth for organic beverages within the market.

“Organic beverages are the fourth-largest organic food category, posting $5.2 billion in sales in 2016 with a growth rate of 8.9 percent,” Haumann explains. “Organic fresh juice drinks, including kombucha, experienced the strongest sales growth. Beside organic fresh juice drinks, other high-growth areas in organic beverages in 2016 included cold-brewed coffee, plant-based dairy alternatives, natural sodas, energy drinks, enhanced water and functional beverages.”

She adds, however, that some consumers still are confused about the benefits of organic versus natural offerings, with consumers having a hard time differentiating between the two attributes.

The association’s 2017 Organic Industry Survey notes that, in 2016, the organic market exhibited consistent growth compared with the downward pressure on pricing that continued to hit conventional markets.

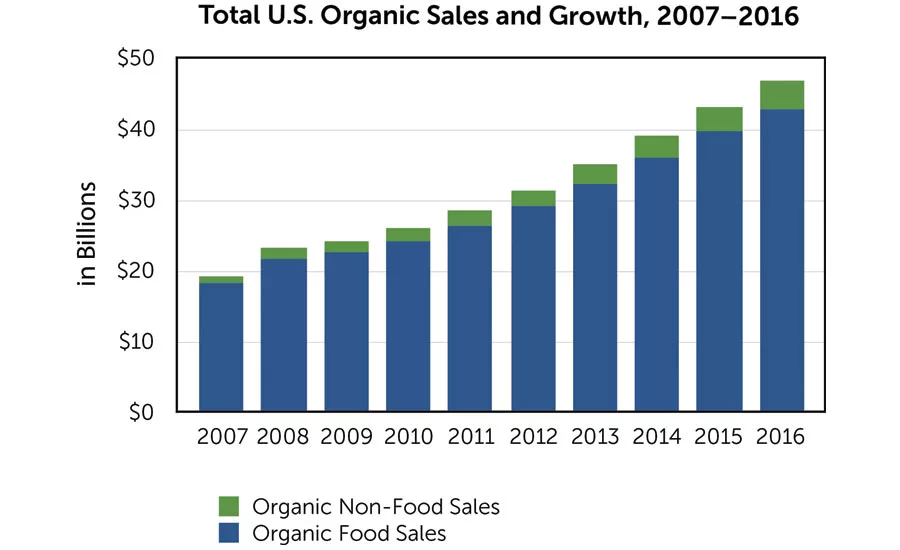

“The organic industry maintained steady growth in 2016, with a rate of 8.4 percent compared to the almost stagnant 0.7 percent growth for overall food and non-food markets,” the survey states. “Organic’s growth translated to $47 billion in sales, an increase of $3.7 billion in sales over 2015.”

The fact that natural and organic foods now are firmly established in mainstream grocers also is shifting the competitive landscape for retailers across the board, according to Packaged Facts’ August report titled “Natural Channel Grocery Shopping.”

“As early as 2014, it was clear that organic foods had become ‘must-have’ items beyond the shelves of natural food stores,” the report states. “… What this means in 2017 is that natural and organic foods can be found in most supermarkets and supercenters, shifting the competitive paradigm from natural food chains pitted against each other into a broader battle for share of the overall marketplace for natural and organic fare.”

Among the trends putting pressure on various retail channels are food deflation driven by heavy discounting, shakeups among major chains, heighted brick-and-mortar competition, and the incursion of eCommerce onto the food retailing landscape, the report states.

For CPG categories, sales growth has been the fastest in the eCommerce channel. “In the realm of groceries and consumables, eCommerce sales rose 21 percent in 2015 to reach $29.5 billion, and this pace of growth is expected to continue through 2020,” it adds, citing Long Grove, Ill.-based Willard Bishop’s 2016 “Future of Food Retailing” report.

Going forward, Packaged Facts’ August report predicts that the natural and organic segments will continue to grow in the low double-digits.

“Packaged Facts estimates that U.S. retail sales of natural and organic foods grew 7 percent on a compound annual basis from 2012 to 2016 to reach $69.4 billion, with average annual growth of 11 percent expected to bring sales to $117.9 billion by 2021,” it states. “By comparison, sales of groceries and consumables overall have been growing by approximately 1 percent to 2 percent annually.”

Packaged Facts’ Lummis suggests that competition and delivery methods will continue to impact the natural and organics channel.

“Even when paying for a membership on Amazon Prime, consumers still feel like they’re getting a deal,” he says. “With three clicks, consumers can have cases of water and heavy bags of pet food shipped directly to their homes, saving time.

”One of biggest challenges for natural retailers is going to be the delivery question,” Lummis continues. “The future is both in-store pickup and home delivery. It’s where the industry is going.” BI

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!