2016 Beer Report: Changes in store for U.S. beer category

Super-premium, flavors helping domestic beer segment

Redd’s Apple Ale expanded its portfolio with the Limited Pick series, which includes Redd’s Cranberry Ale. The brand launched the limited-release beer in February. (Image courtesy of MillerCoors)

Piggybacking off of last year’s positive performance, the U.S. beer market continues to post increases in both dollar and volume sales. According to Chicago-based Information Resources Inc. (IRI), the overall beer category was up 4.8 percent in dollar sales — totaling $33.3 billion — while case sales were up 2.1 percent — more than 1.4 billion — for the 52 weeks ending Dec. 27, 2015, in U.S. supermarkets, drug stores, mass merchandisers, gas and convenience stores, military commissaries, and select club and dollar retail chains.

As Americans flock to the polls this November to elect a new president, consumers also are using their freedom of choice to elect a new way to consume beer. Whether it’s the pending merger between Anheuser-Busch InBev (AB InBev), Leuven, Belgium, and SABMiller plc, London, the growth of U.S. breweries or premiumization trends, changes are in store for the U.S. beer market.

“The U.S. beer category is currently experiencing a major overhaul,” says Beth Bloom, food and drink analyst for Chicago-based Mintel. “While little movement is evident in terms of the overall performance of the category, there are significant shifts happening within. Dollar sales of beer are expected to grow a moderate 4 percent in 2015, amounting to overall gains of 21 percent since 2010. However, volume sales declined during this time, pointing at a shift toward premiumization and the rise of craft beer.

“The super-premium/premium, imported and craft segments have shown growth during the period, with higher price points contributing to dollar sales increases,” she continues. “The total number of U.S. breweries reached a record level in 2015 — pointing to growth. Mergers and acquisitions abound and AB InBev’s acquisition of SABMiller looks set to instigate significant further changes in the coming years and Mintel forecasts the category will continue to post steady gains through 2020.”

However, the AB InBev-SABMiller merger likely will have a different impact on Chicago-based MillerCoors, the U.S. joint venture between SABMiller and Molson Coors Brewing Co., Denver. Following the merger announcement, Molson Coors announced it entered into an agreement to purchase SABMiller’s 58 percent ownership stake in MillerCoors.

Still, the merger of the world’s two largest brewers could have a domino effect. “If the deal gets through regulators during 2016, it will mean that one brewer accounts for almost a third of all beers sold,” says Jonny Forsyth, global drinks analyst for Mintel. “This is likely to stimulate further mergers and acquisitions as global competitors both seek to play catch-up and compete for brands and businesses that the new global mega-brewer is being forced to offload.”

Premium effects

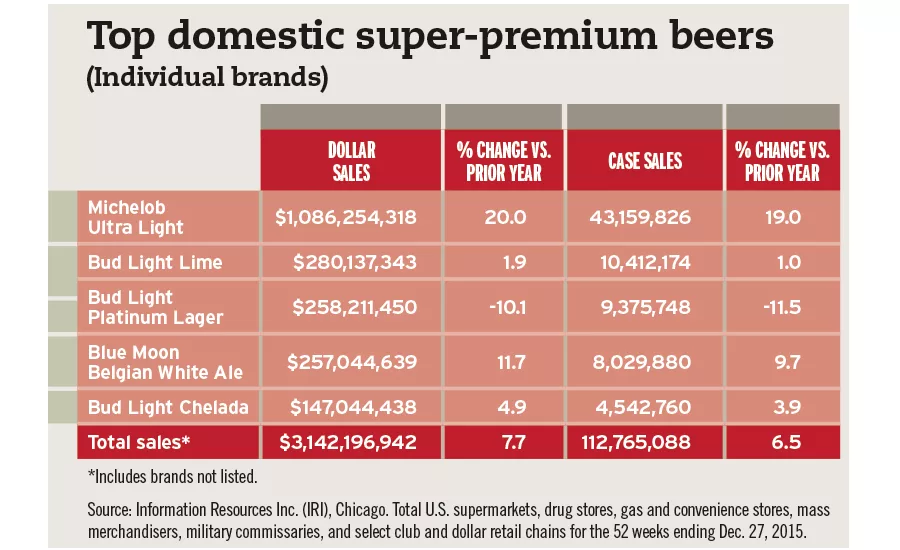

Beyond mergers and acquisitions, the domestic beer segment continues to experience stronger gains from premium and super-premium sub-segments, while sub-premium remains in contraction.

“Similar to other beverage categories, the high-end is driving most of the growth in domestic beer,” says Danelle Kosmal, vice president of beverage alcohol practice for New York-based Nielsen.

To capitalize on this trend, brewers are releasing more flavor options within their super-premium portfolios.

An extension of its Redd’s Apple Ale family, MillerCoors unveiled its Limited Pick series. The special-release ales will feature three new beers — Redd’s Cranberry Ale, Redd’s Blueberry Ale and Redd’s Ginger Apple Ale — throughout 2016. Released in February, Cranberry Ale was the first of the series.

Mintel’s Bloom notes that research shows more consumers are drinking flavored beers, which could bode well for the category. Hard/alcohol sodas fall within that segment, she adds.

In line with these trends, large manufacturers are entering this arena. Anheuser-Busch, St. Louis, released Best Damn Root Beer and Best Damn Apple Ale, while MillerCoors recently launched Henry’s Hard Sodas.

Domestic brands also are competing through marketing campaigns, notes Eric Penicka, research analyst for Chicago-based Euromonitor International.

“Domestic beers are continuing to feel pressure from premium beers (craft/imports); however, they’ve been able to regain some footing with a marketing push focused on their historic relevance in the U.S. market,” he says.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!