What is going on in the US Beverage Alcohol Market?

Alternative adult beverages growing share across total alcohol

Image courtesy of Getty Images

For more than 20 years we have spoken about the growing trend toward easier to drink beverage alcohol products. We tracked them as AAB (alternative alcoholic beverage), products across all non-traditional alcohol forms to include: flavored malt / sugar based products, spirit ready-to-drink (RTDs), wine RTDs, hard cider and wine in can. Some others have used different names in recent years to address the same market. These products generally are in the form of single-serve packages and primarily meant to be consumed without mixing. The movement to these AAB products has accelerated as the overall category has hit critical mass.

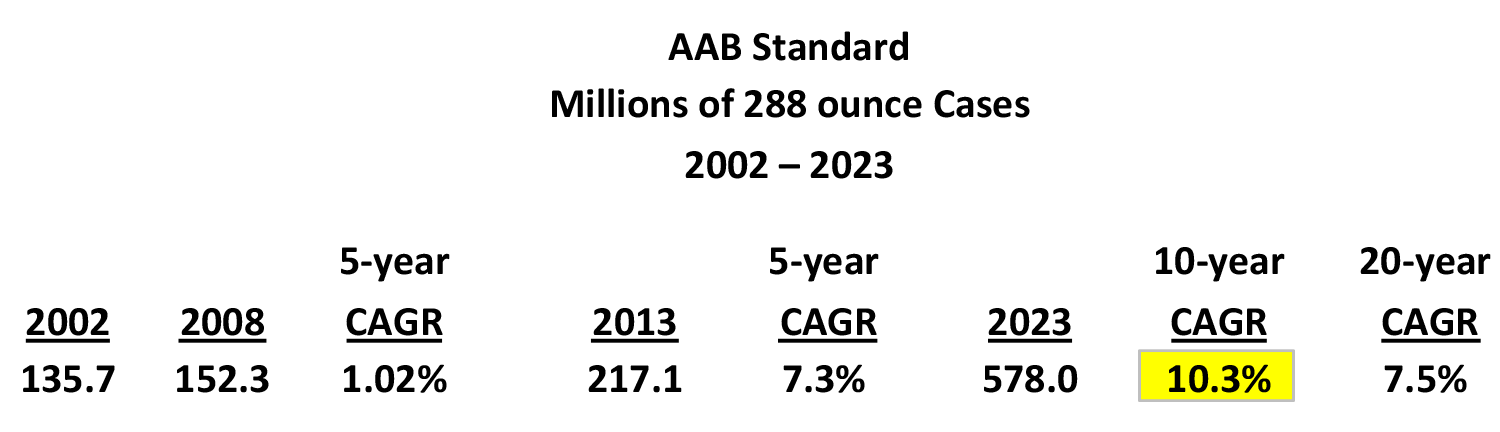

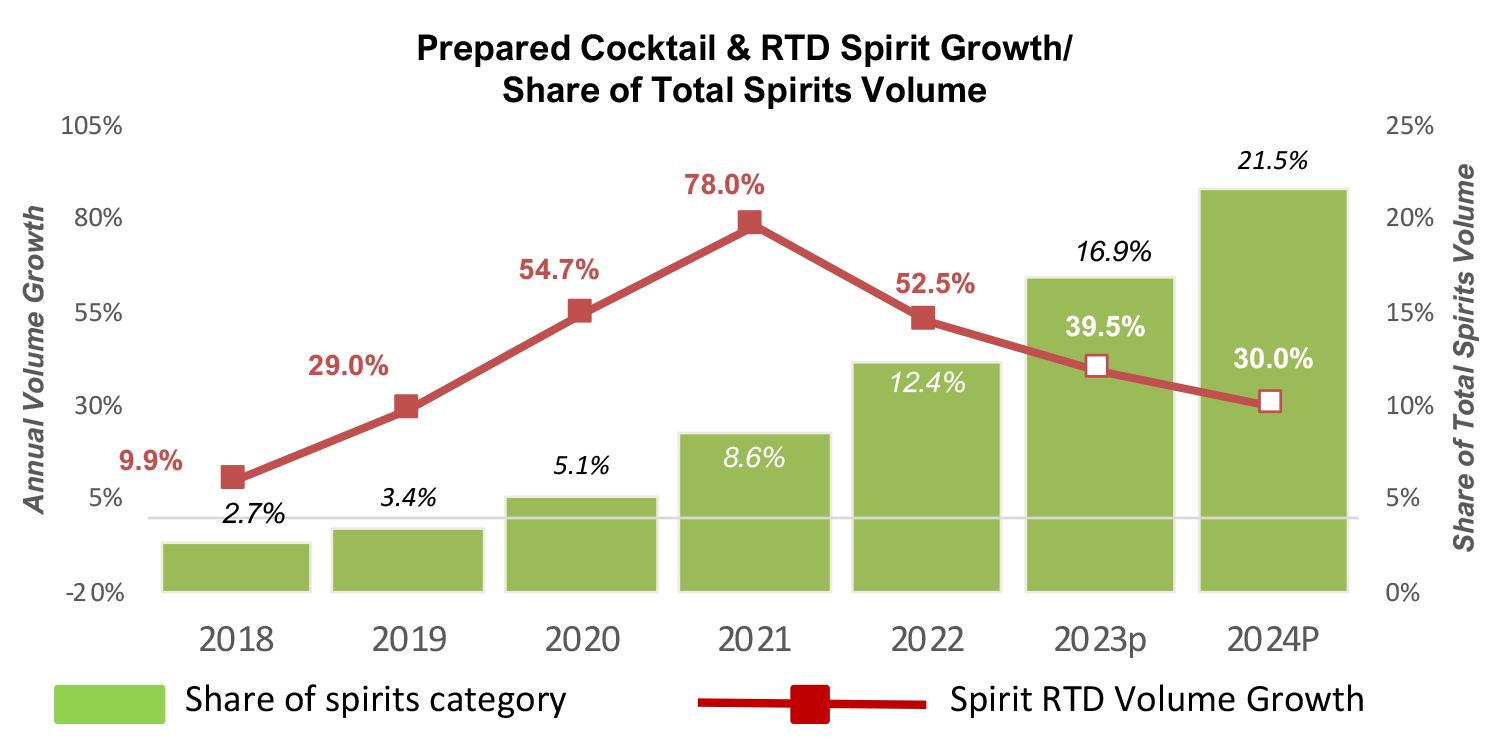

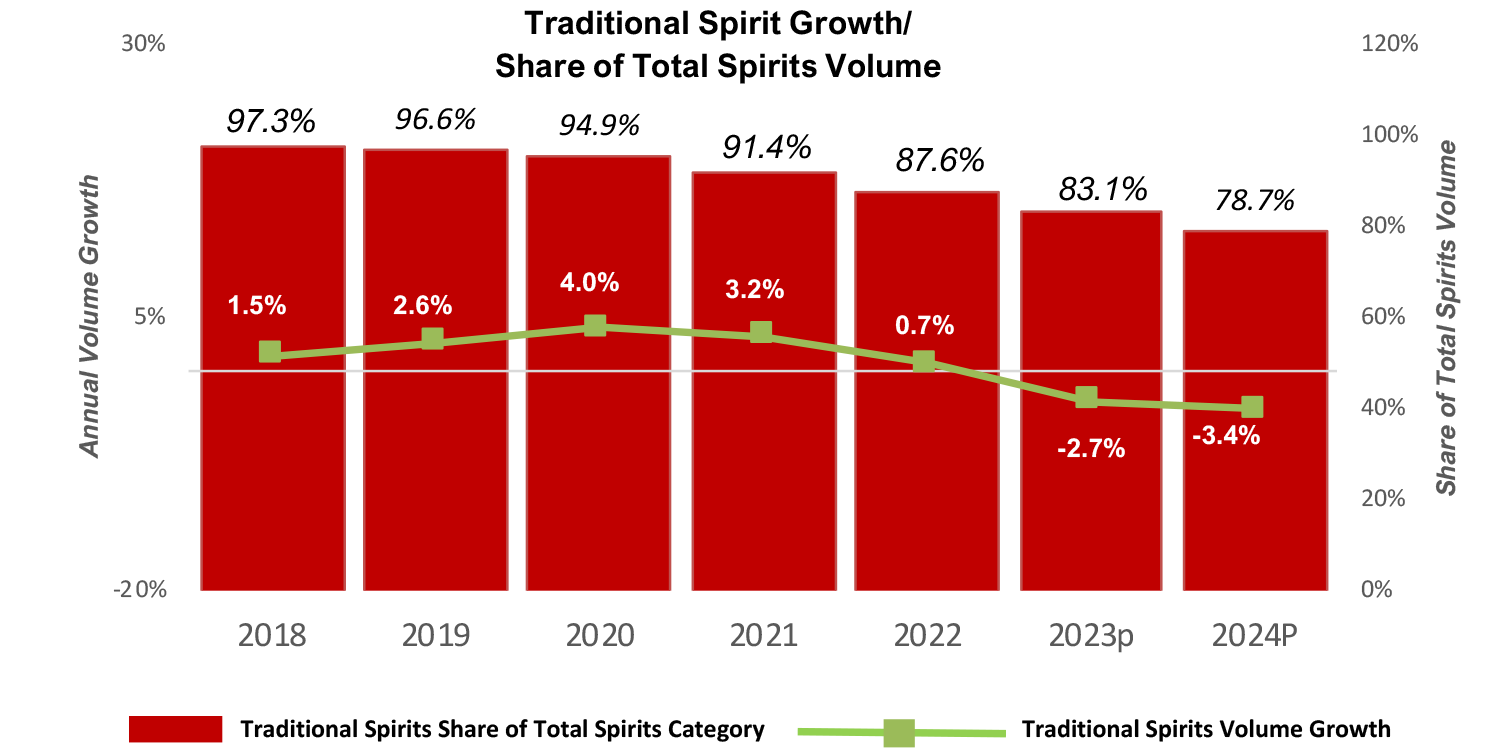

While the AAB market grew by 7.5% a year or 426% in total since 2002, the total beer market has declined more than 5% in total during this period. This disparity underscores the macro movement to these flavored forward, more modern products. We are now beginning to see this bleed into spirits as spirit RTDs have reached scale as the two slides show.

Beginning in 2020, we included cannabis beverages as part of AAB and now refer to it as alternative adult beverages. S&D Insights estimate that cannabis beverages were roughly 18 million cases in 2023. Although there seems to be demand for the product, it has been held back by a very uncertain regulatory environment. Many distributors have hesitated to take on cannabis products. Nadine Sarwat at Bernstein published a report siting several sources which indicate that between 25% and 35% of users of cannabis drink less alcohol. Distributors that sell cannabis beverages, which S&D has surveyed, estimate beverage alcohol sales are reduced by as much as half the amount of cannabis sold to the retail account, i.e., if they sell $5,000 of cannabis beverages into an account, beverage alcohol sales would be reduced by $2,500. It is difficult to estimate what the true impact of legalizing cannabis beverages will have on the U.S. beverage alcohol market, particularly beer, but it seems fairly certain that it will be meaningful.

Most of the innovation in recent years has been focused around AABs from the larger participants in beverage alcohol from distillers to brewers. The two largest beverage companies in Coke and Pepsi are now in the space along with the largest energy drink player in Monster Beverages. This has further driven the AAB category growth versus traditional formats. At one point, the rave was around different beer styles, bourbon varieties, origins for tequila and Scotch and wine varieties. Today, it is how different flavor systems are combined with traditional alcoholic bases to deliver different easier to drink taste profiles. Today, AAB represents 12.6% of total beverage alcohol servings, larger than wine, while tomorrow remains to be seen. As long as marketers continue to invest behind these offerings and focus their innovation efforts against them, the runway for AABs is very long.

The impact on AABs is becoming more apparent as they grow in scale. From only 4.4% of total beverage alcohol servings to 12.6% in 2023 and we project 18.4% in 2027.

Rise of Alternative Adult Beverages - Servings Share 2015-2027P

This rapid growth is coming from all parts of the market and no longer just beer. Spirits and wine AABs are both growing at more than 20% thus far in 2024, while malt/sugar base in growing in the mid to high single digits. At this point, the movement to these type of beverages is yet to abate. We are projecting that AAB will garner another 5 share of adult beverages come 2027 as consumer consumption continues to shift.

Competitively AABs have traditionally experienced rapid growth in a single segment, e.g. wine coolers, malternatives, hard sodas, etc., and then moved to the next, e.g., hard seltzers. Similar to other large categories, the AAB category has generated many sub-segments for which to compete. Each time a sub segment emerges it is bigger than the prior leading sub-segment. This creates challenges to marketers that are accustomed to brands that have long growth curves before maturing. This curve has accelerated dramatically in recent years so as a brand is growing rapidly, marketers need to be developing the next one.

For example, in 2016, hard seltzer was launched. In 2021, both beer and spirit hard seltzer captured over 5% of total beverage alcohol sales dollars, only to begin giving it back to the next high growth AAB segments, hard tea and RTD spirits. One thing for certain, the rapid evolution of AAB ensures that the market will look different in five years than it does today.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!