Cover Feature

IPAs dominate, holding the lion’s share of dollar sales

Beer segment faces increasing competition from beyond beer, non-alcohol

With more than 225 years of collective brewing experience, Delaware’s Dogfish Head Craft Brewery and Belgium’s Brouwerji Rodenbach joined forces to release: Crimson Cru.

Image courtesy of Dogfish Head Craft Brewery

When it comes to the business world, where headwinds can make growth difficult, the late Jimmy Ray Dean, country music singer, actor, businessman and creator of the Jimmy Dean sausage brand, once said: “I can’t change the direction of the wind, but I can adjust my sails to always reach my destination.”

Within the beverage industry, as brands continue to disrupt the status quo on shelf by blending features of two or more categories with each other, experts note that the craft segment is facing strong headwinds, having a tough time keeping pace with the beer category.

Ryan Toenies, client insights consultant at Information Resources Inc. (IRI), Chicago, notes that, although the three-year compound annual growth rate (CAGR) is up 2% for craft beer through the week ending Sept. 11, the overall beer category’s CAGR is up 5.2% for the same time-period.

“The consumer is faced with more choices today than ever,” Toenies explains. “Be it either the traditional, or what we have thought of as the beer and wine segment, the beer segment has now expanded to where those lines have blurred for some of the non-traditional bev alc companies. Non-bev alc companies have partnered-up with the bev alc companies ― Hard MTN DEW is an example of that ― and it has just increased the choices for consumers.

“You now have the increased choices from [ready-to-drink] (RTD) such as Hard MTN DEW or Topo Chico or a High Noon, for example, and that has now squeezed shelf space,” he continues. “Those products have just expanded, so for a consumer line you have those increased bev alc options, but then if you think about the non-bev alc from just what we drink, there’s more choices from a Minute Maid or they have expanded to include near beer lines.”

Scott Scanlon, executive vice president of beverage alcohol at IRI, suggests that where craft is not keeping pace with the beer category, distribution is playing a key role in the segment suffering a little more.

“[I]n my opinion, from looking at the distribution numbers, is the share of distribution shelf,” he says. “The craft segment is continuing to lose year-over-year within the beer category right now and a lot of that is because of the near beer stuff.”

In fact, for the current 52 weeks ending Sept. 11, craft beer is losing share of distribution, down 1.3 share points of total distribution at shelf within the beer category, IRI data shows.

“This is due to the increase of beyond beer and non-alcohol products at retail,” Toenies says.

The power of partnerships, distribution

As smaller craft brewers distribute more regionally and locally, experts note that the larger craft brand families typically do a bit better in dollar sales as these companies are more widely distributed.

Regional craft brewers were down 8.4% in dollar share for the 52 weeks ending Sept. 11, Toenies notes. Meanwhile, “local craft brewers were down the most, minus 11.5% for the same time period, a lot of them [are] losing their distribution,” he says.

Image courtesy of SweetWater Brewing Co.

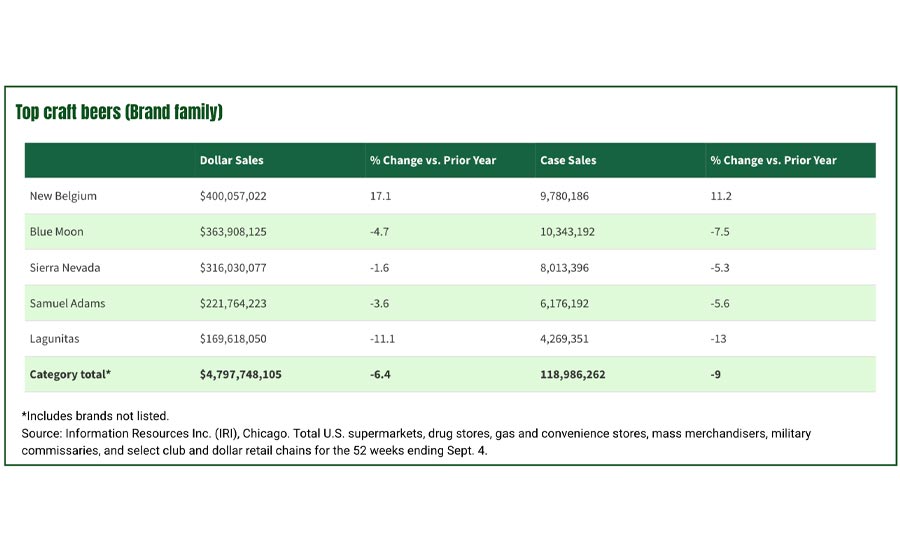

Still, of the Top 10 dollar craft brand families, only New Belgium has positive dollar sales trends, up 17.3% for the 52 weeks ending Sept. 11, Toenies notes.

“Eight of the Top 10 families are losing dollar share of the beer category in the same time period,” he says. “Acquisitions such as New Belgium have added distribution strength to the craft brewer, along with added capital for additional development.”

When it comes to distribution, two variables come into play, Scanlon says. One is the distribution channel, where you have large scale readily implemented, and the other is the relationship with the retailers and shelf availability, he explains.

“It’s much easier to leverage your strength at a large manufacturer to have your product visible on the shelf when you have six or seven other facings than it is to come in as a craft where you’re trying to get your core product on the shelf,” he says.

Moreover, with more brands branching into the RTD, comes more brand partnerships, Scanlon notes.

There probably aren’t as many mergers and acquisitions (M&A) as there have been in previous years, but there definitely are more partnerships, he says. “The companies aren’t truly merging, but they are partnering to create a co-branded product,” he explains.

Further, with a partnered item, Scanlon notes that the distribution and the marketing behind that can create quick buzz. “What’s a better way to get there than the large companies having the large marketing budgets around the market?” he says.

Recently, Dogfish Head Craft Brewery, a wholly owned subsidiary of The Boston Beer Co., joined forces with Belgium’s Brouwerji Rodenbach to release Crimson Cru, a 7.1% ABV blended red ale. After its cross-Atlantic journey, Rodenbach’s Grand Cru is artfully blended with a red ale from Dogfish Head that is infused with sumac and sweet orange peel and dry-hopped with Hallertau Blanc hops, the company notes. The resulting beer is full-bodied and slightly warming with aromas of candied citrus, cherry, caramel and toffee, complemented by malty flavors of stewed fruits, plum, cherry, dried citrus and toffee, it says.

“It was awesome to ― once again ― work with the folks at Rodenbach to create a deliciously complex, multi-continental brew,” said Sam Calagione, Dogfish Head founder and brewer, in a statement, at the time of release. “We worked side-by-side with Rodenbach Brewmaster, Rudi Ghequire on every component of this collaboration; from ingredient sourcing to blending, and even composing the beer’s artful packaging. I’m really proud of the end result and feel that Crimson Cru is a liquid love letter we collectively floated across the Atlantic Ocean and back.”

Room for growth

Known for bringing juicy, hoppy flavors, experts note that IPAs continue to be the largest style within the craft segment, accounting for the lion’s share of dollar sales.

“IPAs are a 46% share of craft and are the dominant style; pale and amber ales, seasonals and wheat ale styles account for 10% share each,” Toenies notes. “Driving those Top 4 styles account for 76% dollar share of craft beer in the 52 weeks ending Sept. 11.”

Yet, the style is slowing down as distribution growth slows for the brands driving this trend, Toenies says.

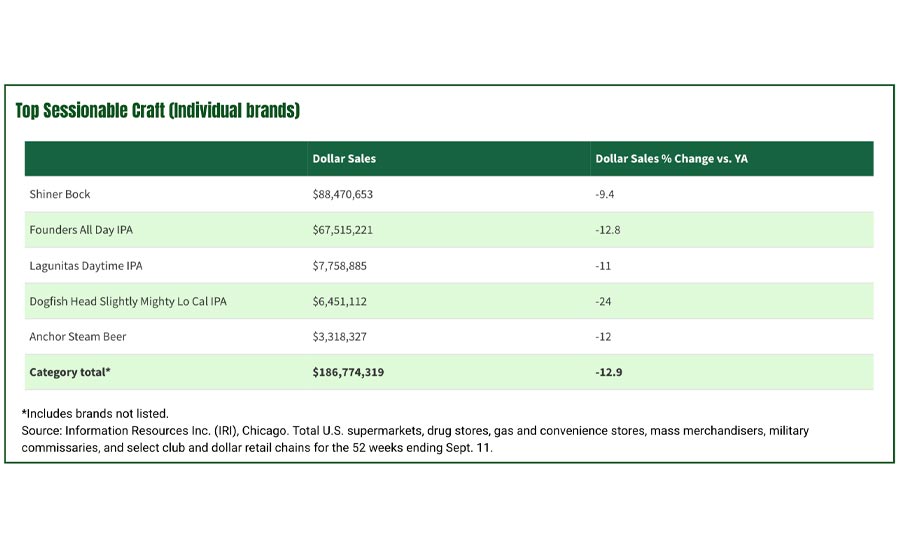

Meanwhile, Top Sessionable Craft three-year CAGR is up 1.5%, but overall dollar sales down 12.9% for the 52 weeks ending Sept. 11, “now not keeping pace with the craft segment,” he notes.

“There could be more opportunities with sessionable, lower ABV, better-for-you, where [the ABV] is closer to like a 4% maybe like a 5%.” Toenies says.

As traditional craft brewers are having success in the seltzer, flavored malt beverage (FMB) and the non- alcohol space, these brewers could have more success in offering lower ABV options as well, he explains.

This summer, Boston-based Harpoon Brewery announced an addition to its League Family with the launch of its first non-alcohol hazy IPA: Open League. Brewed with juicy tropical hops, Open League is a light and refreshing beverage at only 35 calories and less than 0.5% ABV in each serving, it notes. This new, year-round offering is brewed with some of the same “better-for-you” ingredients as Rec. League, like toasted buckwheat, chia seeds and sea salt for electrolytes, the company says.

Image courtesy of Harpoon Brewery

Although the impact of the no-low alcohol trend still is small, Scanlon notes that the growth numbers are large.

“The better-for-you trend has really taken off, just as it has in traditional CPG, so you’re having an additional element claw away at some of that growth that one would’ve normally expected to go to the craft segment,” he says. “Now you have the better-for-you, low ABV that is just another element that’s going to pull those sales down.

“FMBs are picking up a lot right now, they seem to be surging, some of the traditional FMBs as well this year. Before that, it was the seltzer surge,” Scanlon continues. “And now we’ll see pre-mixed RTD cocktails taking some away from the segment as well.”

Moreover, Scanlon points to current economic conditions, which might further affect the craft segment.

“The age-old question continues to be if premiumization is going to continue or is that out,” Scanlon says. “And craft is not immune from that discussion. I am not seeing it, yet. The data has not reflected that we’re seeing it pull back from premium, I think it is too early to tell.

“As many economists are finding, I think a lot of that is going to depend upon the job data,” he continues. “And the economy can pull back, which we’ve seen in the past, but in order for us to have a 2000 or a 2007-08 type of experience where we see somewhat of a pivot to value oriented brands, then I think we would have to see a deteriorated jobs market.”

Further, as beverage alcohol has always been a market where anything new really develops beyond on-premise, Scanlon notes that that narrative has changed with seltzers and RTDs.

Although seltzers and RTDs were born on-premise, “they’re still trying to get their way into on-premise in many respects,” he explains. “We have created that disruption and COVID just magnified that because there was very little on-premise certainly in many regional areas. So now it’s trying to get back to that and it will be interesting to see.”

Where beverage trends can affect the craft segment, Toenies notes that the betterment trend will only continue to drive consumers to the no-low alcohol space. Yet, craft brewers are seeing success in this space, he says.

“The beyond beer trends will continue to disrupt the craft environment, but craft brewers are showing they can win in this space as well if they innovate wisely,” he concludes.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!