Cover Feature

Cannabis beverages look to overcome challenges to expand market

Millennials account for largest segment of cannabis users, data shows

When Washington and Colorado became the first states to legalize recreational marijuana in 2012, many analysts pondered what potential this new consumer market would have. Based on findings from the February 2022 Market Forecast from BDSA, Louisville, Colo., it’s safe to say that cannabis is a market in high demand.

For 2021, total legal U.S. cannabis sales were estimated to be $24 billion, with $10 billion from the medical channel and the remaining $14 billion coming from the adult-use channel, explains Jessica Lukas, chief commercial officer with BSDA, citing its February report.

The future for cannabis looks to continue its upward trajectory with BDSA forecasting total U.S. cannabis sales to reach $28 billion this year, and grow to $46 billion by 2026, which would be an approximately 92% increase from its estimated 2021 performance.

Although U.S. cannabis sales is poised for steady growth, the future for beverages in this market still is in its early stages.

“Edibles were estimated to make up 15% of total legal sales in 2021,” Lukas explains. “The beverage subcategory represents a small share of the edible category, with BDSA Retail Sales Tracking showing that beverages made up 5% of total edible sales across BDSA tracked markets in 2021.”

Through its 2026 forecast, BDSA projects that edibles will remain around 15% of the total U.S. cannabis sales.

In its March 2021 report titled “Medical & Recreational Marijuana Stores,” Los Angeles-based IBISWorld highlights that edible and ingestibles offer consumers an entry point into cannabis that they are comfortable with. As such, the market research firm expects the segment to continue to grow.

“Edibles can take the form of food, extracts and oils, and range from marijuana-infused mints and candies to baked goods and beverages, along with many other products,” the report states. “Over the five years to 2021, edible marijuana products have grown rapidly as a share of industry revenue. Edibles account for an estimated 18.4% of total retail sales in 2021, but are expected to consume a larger share of total retail sales over the five years to 2026.”

Although cannabis-infused beverages can offer consumers a delivery model that they are comfortable with, BDSA’s Lukas notes the beverage format will be challenged by the convenience and portability that other edibles like gummies can offer.

“Cannabis beverages offer a familiar form factor that some consumers may gravitate toward, and effect-related benefits such as fast-acting effects, but cannabis beverages are unlikely to be a dominant edible subcategory moving forward,” she says. “One reason for this is the category dominance of candy edibles, particularly gummies, which have an advantage over beverages because they offer convenience and portability, two factors that are top product choice influencers according to BDSA Consumer Insights. Another reason is that cannabis beverages present more logistical issues to distributors and retailers, as most beverage products are more costly to transport and store at retail than smaller and lighter edible form factors.”

Despite this competition, cannabis beverages are finding ways to differentiate themselves from other edible markets.

“Among beverage products tracked by BDSA Retail Sales Tracking, there is a trend of citrus-flavored beverages making up more top products across all BDSA-tracked markets than any other beverage flavor,” Lukas says. “This is in contrast to the gummie edible category, where berry and watermelon flavors are the most common among top products.”

Recognizing the potential across all edible segments, Jones Soda Co., Seattle, recently entered the cannabis-infused beverage and edibles business with the release of the first products from a new division operating under the Mary Jones brand. The launch portfolio of 16 SKUs includes single and multi-dose infused sodas as well as syrup and gummies.

Initially launching in California, all products are available in Jones’ fan-favorite Root Beer, Berry Lemonade, Green Apple and Orange Cream flavors, with a rotating selection of seasonal and limited-edition flavors planned for future release. The Jones flavor science team designed each of these products to recreate Jones popular mainline soda flavors, it says.

“The Mary Jones brand is a game changer because, unlike every other company in the space, we bring an iconic brand with an equity that eclipses any current cannabis brand in the market, passionate fans who love our signature flavors, and a 25-year history of having fun with consumers by putting our fans' photos on our labels, their quotes under our bottle caps and being available in record shops as often as the grocery store. This is real earned credibility you can't fabricate,” said Bohb Blair, chief brand officer for Mary Jones Cannabis Inc., in a statement. “With all of these advantages, our irreverent personality and putting a cannabis twist on our brand traditions, we believe we are uniquely positioned to dominate the category.”

Beverage-makers also are taking a cue from the seasons as they expand their flavor options. Happi, Birmingham, Mich., launched its newest flavor ― Pomegranate Hibiscus ― in select provisioning centers. Made with organic pomegranate, lemon, agave nectar and hibiscus, the cannabis-infused sparkling water contains 2.5 mg of THC and is made with simple ingredients and just 25 calories in each 8.4-ounce slim can.

“Among beverage products tracked by BDSA Retail Sales Tracking, there is a trend of citrus-flavored beverages making up more top products across all BDSA-tracked markets than any other beverage flavor. This is in contrast to the gummie edible category, where berry and watermelon flavors are the most common among top products.”

- Jessica Lukas, chief commercial officer with BSDA

“We are proud to give Michiganders something to celebrate this spring with the launch of our latest flavor, Pomegranate Hibiscus. Enjoying the big and small occasions of spring — warmer days outside with family, exploring farmers markets — after the long Michigan winter are best honored with a Happi in hand,” said Lisa Hurwitz, president of Happi, in a statement. “Through our distribution partners, we look forward to a happy spring season.”

Deeper understanding of cannabis

As beverage-makers look to further the category’s presence in the overall cannabis market, helping to educate consumers about cannabis and hemp will play an important role going forward.

“According to BDSA Consumer Insights research from fall 2021, 20% of CBD consumers claimed to have ‘expert’ knowledge of cannabinoids (including THC and CBD),” BDSA’s Lukas says. “Twenty-five percent of CBD consumers claimed to have a basic understanding of cannabinoids and understand the various compounds and their applications. Thirty percent of consumers claimed to have a basic understanding of cannabinoids, but were not familiar with the various compounds and applications.”

Lukas explains that there are more than 100 cannabinoids produced by the cannabis plant, but CBD and THC are the most commonly used compounds.

“THC, the cannabinoid most associated with cannabis, is responsible for cannabis’ intoxicating effect. THC is also used for in a variety of therapeutic applications, including as a pain reliever, nausea reliever, sleep aid, and appetite stimulant,” Lukas says. “Unlike THC, CBD is not intoxicating. CBD is also used for several therapeutic applications, such as a treatment for pain, inflammation, nausea, migraines, anxiety and seizures. In 2018, the Food and Drug Administration approved Epidiolex, the first prescription medication containing CBD, as a treatment for rare forms of epilepsy.

“Both THC and CBD are found in the Cannabis sativa plant, which the cannabis and hemp plants come from,” she continues. “While CBD is found in both hemp and cannabis plants, hemp produces very small levels of THC. Hemp, which was legalized in the U.S. by the 2018 Farm Bill, may legally contain up to 0.3% THC.”

Whether it is CBD, THC or one of the emerging cannabis compounds, consumers are relying on personal contacts to learn more about these ingredients.

“Across all CBD consumers, BDSA Consumer Insights data from fall 2021 show that the most common information source for CBD is friends and family, followed by cannabis dispensaries,” Lukas explains. “BDSA believes that mood/effect-driven product labeling and marketing will be a major trend in the cannabis industry going forward, which will be a main factor driving consumer knowledge of cannabinoids and their various effects.”

As consumers gain knowledge of these effects, experts note that they will become better acquainted with the medical and recreational benefits that cannabis supporters tout.

“BDSA Consumer Insights data from fall 2021 show that the top claimed reasons for consuming are to relieve pain, sleep better, and relax/be mellow,” Lukas says. “A desire to manage anxiety and improve one’s quality of life were also commonly claimed reasons for consuming cannabis.”

However, cannabis’ status with the federal government for THC-containing products will keep its products in dispensaries and out of traditional retail outlets in the near term. The same cannot be said for CBD-containing products.

“While cannabis (products containing [greater than] 3% THC) is likely to remain out of CPG channels until federal legalization and descheduling of cannabis from the Controlled Substances Act, the barriers for CBD to enter the CPG universe are lower,” Lukas says. “The Farm Bill legalized the production of hemp-based CBD at the federal level, but without FDA guidance allowing CBD and a food and beverage additive, the bulk of CBD sales are expected to go through the dispensaries and eCommerce channels.”

Cannabis’ evolution

Although the federal legal status of cannabis remains in limbo, research shows that consumers are much less conflicted.

In November 2021, Gallup released its annual poll on the U.S. support for legalizing marijuana. The poll’s record-high level of 68% of Americans in favor of legalization was maintained for the second year in a row.

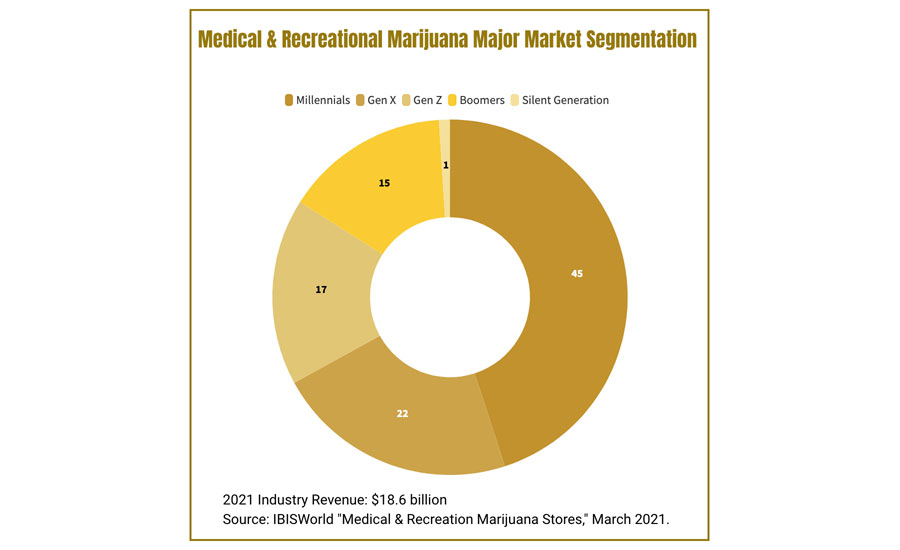

According to IBISWorld’s report, demographic segmentation of medical and recreational marijuana’s consumer base shows that millennials (which it defines as ages 25-40) are the largest group based on 2021 revenue followed by Generation X and Generation Z.

For Generation Z (defined as ages 9 to 24), the report highlights that even though the majority of this demographic is below 21, research shows this generation is a proponent of legalizing marijuana and as such will see its market share grow over the years.

“Since this generation is largely accepting of legalizing the medical and recreational use of marijuana, they comprise a significant amount of industry revenue, despite the fact that the majority of ages in this segment are below 21,” the report states. “In 2021, Gen Z consumers are expected to account for 17% of total industry revenue. When breaking out usage of medical marijuana versus recreational marijuana, Gen Z is expected to account for 17% in both markets. This market segment is expected to continue to grow over the five years to 2026 since consumers in this bracket are aging into the legal age range every day.”

However, with all millennials legally of age, this demographic remains the top segment for marijuana use.

“In 2021, millennials are expected to account for 45% of total industry revenue,” the report states. “Similar to Gen Z, consumers in this age group are increasingly in support of legalizing medical and recreational marijuana use. In fact, millennials are expected to comprise a larger portion of the recreational marijuana market than the medical marijuana market. In 2021, millennials are estimated to account for 42% of the medical market and 48% of the recreational market. This market segment is expected to continue to grow over the next five years as consumers continue to become more accepting of the industry and legalization throughout the country increases.”

As support for legalization status mounts though, experts note that to become a mainstream product in the consumer packaged goods arena, adjustments should be made to engage with consumers.

In a September 2021 Insights by Shane MacGuill and Spiros Malandrakis with Chicago-based Euromonitor International titled “From Taboo to Typical: Global Cannabis Comes of Age,” the analysts note the importance of tailoring brand propositions to specific demographics.

“From identifying the cannacurious cohort to expand penetration and reach to focusing on seasoned consumers to allow for connoisseurship and premiumization to add value, diligent segmentation will be another sign of the industry’s transition into mature FMCG territory,” the two state. “Euromonitor International’s surveys are also shedding light into key perceptions, concerns and patterns.

“For example, 79% of cannabis consumers in U.S. legal states consider strength to be an important product attribute followed by price (70%) and strain (66%) ― a fact that highlights the still simplistic and embryonic nature of buying behaviors, a situation that is in many ways akin to alcohol consumers choosing brands purely based on ABV content,” they continue. “But on the CBD front, education also remains essential with 43% of global respondents saying that they do not see a clear need to use CBD.”

As more consumers accept cannabis as part of the CPG market, the messaging and look of its segments will likely evolve with that acceptance.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!