Almond, coconut, cashew milks gain in dairy alternatives

Segment mainstays down in volume, sales

Despite seeing significant growth during the 2010-2015 timeframe, the dairy and dairy alternatives category has seen a deceleration in growth, according to experts. Although the growth will be at a slower pace, the category still is expected to continue gaining share in the beverage market going forward.

“Packaged Facts projects the dairy and dairy alternative beverages market will reach $31.5 billion by 2019, up by about a third from its current level of nearly $23.8 billion [in 2015],” reports the Rockville, Md.-based market research firm in its April 2015 report “Dairy and Dairy Alternative Beverage Trends in the U.S.” “Growth should be steady and increasing as new and innovative products continue to enter the market and premium products achieve more widespread penetration in the market. The compound annual growth rate (CAGR) for the five-year period [2015-2019] would be 5.8 percent.”

Although the market is seeing interest from large beverage and non-beverage-exclusive companies, it still is dominated by private-label brands, the report notes. Private-label products in the dairy and dairy alternative beverage category account for half of the overall sales, including the refrigerated side of the market. However, branded dairy and dairy alternative products dominate the shelf-stable segment of the market, it states.

Among the brands maintaining market share, Denver-based WhiteWave Foods Co., which was recently acquired by Danone, Paris, holds the majority of the share. “WhiteWave has the largest share at 13 percent of overall sales and also of refrigerated sales as well as a 22 percent share in the shelf-stable market,” the Packaged Facts report states. “It is the only market participant with a double-digit share in the overall and refrigerated markets. However, Nestlé and Dr Pepper/Snapple have double-digit shares in the shelf-stable market.”

New alternative leaders

As the dairy alternatives segment has grown, it also has evolved and seen new leaders come to the forefront. Currently, almond milk is driving the dairy alternatives segment, according to Gary Hemphill, managing director of research at New York-based Beverage Marketing Corporation (BMC). Although growth in the dairy alternatives segment slowed in 2015, it will continue to see modest growth going forward, he says.

According to John Crawford, vice president of client insights for dairy at Information Resources Inc. (IRI), Chicago, the plant-based/alternative beverages segment was up 5.2 percent from the previous year reaching $1.7 billion in the 52 weeks ending Sept. 4 in total U.S. multi-outlets and convenience stores. The dairy alternative segment’s volume grew 5 percent to 242.2 million gallons in the same timeframe, he adds.

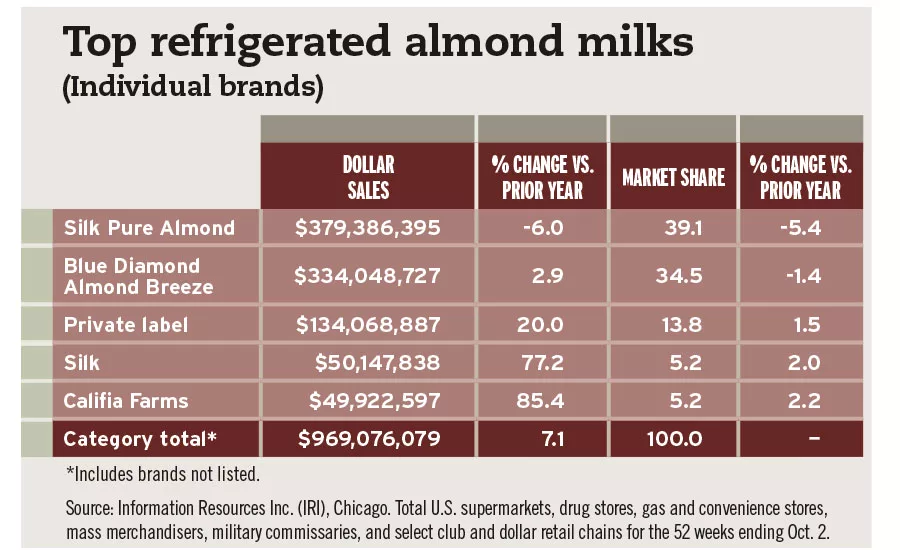

Crawford says that almond milk accounts for 68 percent of the total plant-based/alternative beverage segment in volume and is up 8.5 percent to 165.3 million gallons while sales are up 7.9 percent to $1.1 billion for the 52 weeks ending Sept. 4.

Packaged Facts also notes the impact of almond milk. “Strong growth in the almond milk segment is the single most significant development in market trends in dairy and dairy alternative beverages,” it states.

Yet, BMC’s Hemphill notes that with the growth of new alternatives, the previous mainstays of the category are losing share. “Within the market, the dynamics have shifted,” he says. “At one time, soy defined virtually the entire dairy alternative category,” he says. “Today, there are many other dairy alternatives — almond, rice, hemp and others. With this, soy has slipped in popularity.”

Chicago-based Mintel also notes this trend in its April 2016 “Non-Dairy Milk – US” report. According to the report, soy milk made up approximately 19.3 percent of the market in 2015, and the lost sales in this segment have hindered overall category growth. “Soy milk is forecast to be surpassed by the ‘other’ non-dairy milk segment by 2017 and coconut milk by 2018, as consumers look to other plant-based milks to meet their drinking occasions,” the report states.

IRI’s Crawford notes that the soy milk segment was down 9.5 percent in sales, dropping sales to $300 million, while volume was down 10.3 percent to 44 million gallons for the 52 weeks ending Sept. 4.

However, almond milk isn’t the only dairy alternative making waves in the segment. Sales of coconut and cashew milks also are increasing, albeit from a smaller base. According to Crawford, coconut milk sales were up 11 percent to $163.8 million and volume increased 10.8 percent to 16.2 million gallons for the 52 weeks ending Sept. 4.

Cashew milk experienced even greater growth with sales growing at 58.1 percent to $53.6 million and volume up 56.9 percent to 8.2 million gallons for the same timeframe, he says. Crawford adds that in 2014, cashew milk volume was a mere 233,000 gallons.

“Plant-based/alternative beverages continue to grow with new varieties coming along all the time,” he says. “Cashew milk is hot, and banana milk is a new variety that we will see in the coming years.”

Experts say that the market will be driven by further innovation with other plant-based alternatives that are garnering consumer attention. “Sales of plant-based dairy alternative beverages have grown rapidly over the last few years, especially those of almond milk. In addition, consumers are clearly intrigued by other plant-based beverages that are being introduced in greater number including those made from cashew, quinoa, sunflower and flaxseed,” the Packaged Facts report states.

As the number of dairy alternatives grows, beverage-makers have begun to use combinations of various alternatives in their new product development. “Processors are also offering blends of two or more plant-based ingredients and flavors,” the Packaged Facts report states. “Almond-coconut combinations are a basic, while more ambitious mixes are being launched with ingredients such as chia, quinoa and hazelnut added to coconut, almond and rice drinks.”

The path to success

Several trends are contributing to the growth of the dairy and dairy alternatives category, including the increasing release of seasonal and limited-edition flavors to attract consumers to products, according to Packaged Facts’ report. “The development of more flavored varieties has been among the leading product strategies marketers have been employing to boost sales,” it states.

However, IRI’s Crawford notes that when it comes to flavors, consumers are divided nearly 50/50. But he says that several flavors are trending in both dairy- and plant-based beverages, including vanilla, pumpkin and banana.

Within the dairy and dairy alternatives category, innovation and fortification will be essential for future success, experts say. In its report, Packaged Facts highlights that high-protein offerings are growing within the category, most notably via smoothies and shakes.

When it comes to the dairy alternatives segment, Mintel notes several attributes that are trending in its report, including no artificial ingredients, no artificial sweeteners, non-GMO and dairy free.

It also highlights that innovation with flavor, function and usage occasions will be key aspects for growth. “Consumers are mostly likely to say extra protein and added vitamins and minerals would encourage them to increase their non-dairy milk consumption. This aligns with consumers’ top reasons for drinking non-dairy milk,” it states.

Additionally, the report states that 21 percent of non-dairy milk drinkers are interested in the energizing benefit of alternative beverages. On the flip side, 16 percent of non-dairy milk drinkers are interested in alternatives that help promote relaxation, it adds.

In a January survey of 2,000 Internet users aged 18 and older, extra protein ranked among the top attributes that consumers say would encourage them to drink non-dairy milk. BI

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!