How to grow private label brands

Innovation, differentiation key for category success

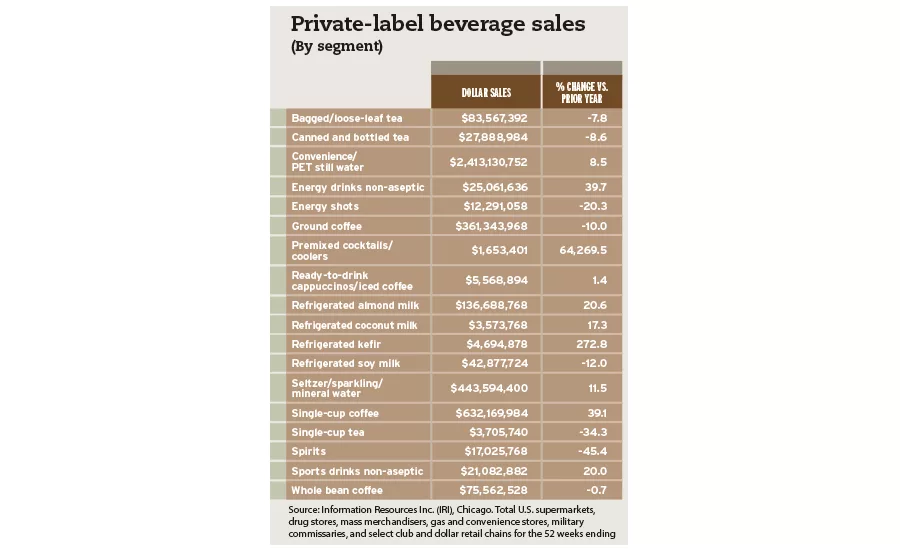

After a boom in growth in the early 2000s, the private-label consumer packaged goods (CPG) market has experienced stagnant growth since 2015, according to market research experts. Although the private-label beverage market has maintained its share of the market — and even experienced some growth — experts say that the market is expected to grow at low rates.

“Today, private-label brands account for 14.5 percent of CPG dollar sales and 17.1 percent of unit sales,” says Susan Viamari, vice president of Thought Leadership at Chicago-based Information Resources Inc. (IRI). “… In the beverage department, private label holds

9 percent share of unit sales. During the past year, share has actually ticked up, driven by retailers placing more emphasis on expanding their private-label beverage benefits beyond simple thirst quenching. By delivering against sought-after benefits, such as nutritional enhancement, workout recovery and energy enhancement, emerging private-label beverage categories — liquid drink enhancers (plus 4.8 points), bottled water (plus 1 point) and coffee (plus 0.7 points) — have seen private label share jump.”

According to Chicago-based Mintel’s February report “Private Label Food Trends – U.S.,” sales of private-label food and beverages increased by 2 percent in 2015. The market research firm expects a similar rate through 2020.

However, continued innovation has the potential to drive the category, experts say. “Private-label beverages must compete as true brands — which they really are these days,” IRI’s Viamari says. “Innovation needs to differentiate from name brands, rather than taking a follower approach.”

Hope Lee, senior global beverage analyst for London-based Euromonitor International, notes that the market does not yet have a vast selection of options. “The interesting trend, in terms of private labels sales, lies in the different percent-holdings of overall soft drinks and health-and-wellness soft drinks sales,” she says. “Our health-and-wellness database shows a disparity in private labels holdings in different markets. For example, in the U.S., private label held 8 percent share in overall soft drinks, while health-and-wellness soft drinks accounted for over 6 percent by retail value.”

In order to compete in the marketplace, experts highlight several areas where innovation and communication can drive the private-label market forward. In its report, Mintel notes that consumers can be hesitant about the transparency and trustworthiness of some store brands, most notably regarding products with better-for-you and organic claims.

“More than three-quarters of buyers say they would like to see more transparency from store brands about who makes them, how they are produced and what their origins are,” the report states. “More than half agree that national brands do a better job of relaying this information.”

Additionally, the market research firm notes that millennials are more likely than other demographics to trust store brands if they provide transparency. “Given that millennials are attracted to exclusive brands that lend a sense of uniqueness to the buyer, store brands have an opportunity to target millennials with better marketing messages and brand backstories that will resonate with this group,” the report states.

In fact, Mintel's report highlights that millennials are more likely than non-millennials to dedicate a significant portion of their baskets to store brands. Additionally, the demographic has a preference for value products and a willingness to spend more on premium brands, meaning they likely will buy the value and premium store brands, the report notes.

In its November report titled “Private Label: The Journey to Growth Along Roads Less Traveled,” IRI says that a notable portion of private-label growth is coming from premium-tier products, but that all three levels of private-label products are important to drive sales. “While premiumization and differentiation are not synonymous, both are essential, and retailers that bring premium products to market are often creating a unique draw for shoppers of that category,” the report states. “Retailers must work hard to continue to optimize their private-label strategies, finding the right assortment of value, mid-tier and premium solutions that, taken together with national brands, offer their customers the best value across CPG categories.”

IRI's Viamari adds: “New growth is going to come from premiumization and differentiation. A critical step to growth is to stem the tide across categories where private-label share is high, but on a downward trend. … Understanding where the losses are coming from — dollars, volume or both — is an essential first step, since plans to protect and grow will depend on drivers of loss.

“Success is also about taking a new direction,” she continues. “Across a wide swath of categories, private-label growth is healthy. These categories bring great opportunity for retailers that are willing to step outside the traditional private-label box and diversify into new area. Retailers cannot afford to miss the boat across these opportunity categories, especially where growth is accelerating.” BI

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!